UFE Faces the Heritage Foundation on the Estate Tax

Point: Why America Needs a Strong Estate Tax

By Lee Farris

"America is a tremendous nation that faces huge challenges over the coming years. Millions have lost their jobs and homes during this economic crisis, and our nation’s long-term budget is on an unsustainable path.

Despite these facts, there are still some who want to end the estate tax, which would amount

to yet another irresponsible tax break for the wealthy. Sadly, for some of our elected leaders, like Senators Kyl and Lincoln, passing new tax cuts for wealthy trust fund heirs is a higher priority than revitalizing our economy or balancing our budget.

Why do we need an estate tax? Our government plays a vital role in promoting individual opportunity and national prosperity. Simply put, taxes are the price we pay to live in a stable, secure and thriving society with a decent quality of life. The estate tax generates billions in revenue from those most able to pay. The wealthiest Americans have benefitted the most from the investments that our country has made in an educated workforce, reliable transportation, technology and a legal system that makes commerce possible.

Middle class Americans are finding fewer opportunities for success because education and other paths to advancement are increasingly out of reach. The estate tax helps to even the playing field by slowing the concentration of power in the hands of those born into great wealth. [...]"

Read the full op-ed by Lee Farris (PDF 1.1 MB) - see p. 8

Read the Counterpoint by William Beach (PDF 260 KB) - see p. 9

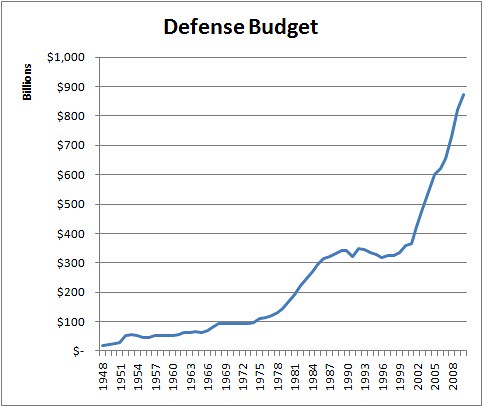

Deficit Hawks Should Eye the Defense Budget

As the debate rages in Congress between deficit hawks and legislators who want to invest money to create jobs, one important point of common ground is being overlooked. The two sides should be able to come together to responsibly downsize America’s bloated defense budget.

Conservative estimates of savings is $1 trillion between 2011-2020. Some of the savings could go to deficit reduction and some towards job creation. Best of all, it's a values-based reprioritization of America’s investments away from guns and back to butter.

Chart h/t Campaign for America's Future

Change Comes to E-News

E-News is changing, and we want your input. As part of a series of upgrades and improvements that we're making to our website, we are retooling the way we produce and present content in our E-News updates. All of our E-News stories are now available live on our website. We're posting new content throughout the month, so you can check in anytime for the latest updates.

Now that we've changed E-News, it's time to rename it. We want your suggestions on what the new E-News will be called. Take a look around. Read the stories. And shoot us an email ([email protected]) with your idea for a new name (or any other thoughts you might have about E-News).

Enjoy the new E-News and thank you for your input.

Carrying Their Own Tax Weight?: High Finance and Carried Interest

The US Senate is combing through the American Jobs and Closing Tax Loopholes Act of 2010 this week. Included in that bill is a provision to close the loophole on what's called "carried interest," which is where most of the income of hedge fund and private equity firm managers comes from.

About the loophole: mega-rich financiers' incomes are a percentage of their funds' annual profits. Our friends at Citizens for Tax Justice explain that managers of various investment partnerships are generally compensated with a "two and twenty" system–that is, they receive a 2% management fee and 20% of all profits of the investment, even if they didn't contribute any funds up front. They claim that income to be capital gains, distinct from earned income, which is therefore subject to the much lower capital gains tax rate of 15% (vs. the top income tax rate of 35 percent).

Ergo, billions of dollars are lost each year to insufficient and unfair taxation on the incomes of these investment banking leaders. Closing this loophole could generate an estimated $25 billion in federal revenue over 10 years.

Len Burman, fellow at the Brookings Institute, had this to say on NPR's Morning Edition:

"It's a huge windfall to some of the best-off people in society, [...] High-income people are supposed to be taxed at the highest rates, 35 percent, [...] But people who are lucky enough to be in the private equity or hedge fund business get their income taxed at a 15 percent rate."

Despite popular anti-Wall Street sentiments and broad, multi-class support for increased taxes on America's wealthy, closing the carried interest loophole is not guaranteed. Alan Sloan gives a personalized take in the Washington Post:

The legislation, introduced by Rep. Sander M. Levin (D-Mich.), calls for private-equity firms, venture-capital firms and real estate investment partnerships to have half their carried interest income treated as capital gains in 2011 and 2012, and 25 to 45 percent of it to be treated as capital gains from 2013 on. [...]

Next year, with tax rates on regular income and capital gains set to increase, the carried interest types' 50-50 split would give them an effective tax rate of 31 percent, rather than the 20 percent capital gains rate. Now, take me, someone who makes a (low-) six-digit income but is stuck in the phaseout bracket of the alternative minimum tax. If my income were split 50-50 next year, my rate would be 32 to 33 percent. I'm well-off, but far from rich by any definition except the Obama administration's. So my sympathy for private-equity types paying higher taxes on their carried interest income is, shall we say, extremely limited."

Some feel that this proposed tax change would stifle industries other than high finance. In the Morning Edition story we cited above, John DeBoer, president of the Real Estate Roundtable, argues that nearly half of US investment partnerships are in real estate, and that increased taxes on developers would prevent a rebuilding of the struggling sector. This and every other anti-tax argument in the context of the carried interest debate don't come as a surprise.

This particular move to even the tax playing field has and will continue to draw criticism from many different directions–including those dreaded and well-funded industry lobbyists. But, we can rest a little easier, as Linda Beale has provided a sensible analysis to help us through most of it. Here's a quick synopsis:

1) Any economic justification for privileged treatment of fund managers is absurd. (They'll still make boatloads of money, even if they have to pay taxes like average Americans.) And, this won't be catastrophic to investment partnerships. (Most of these folks aren't going to quit doing their jobs simply because they're taxed like ordinary people.)

2) Any provision that splits the rate structure (like Rep. Levin's) is arbitrary, creates undue complexity, seems to ask for folks to game the system, and would, according to Beale, only serve as a pacifier for certain high-wealth campaign contributors.

3) Any half-baked measure that continues to favor fund managers is only a sign that "the House and Senate are willing to sell out ordinary taxpayers and continue to favor the wealthy and that fairness loses when the House or Senate is thinking about campaign contributions."

4) Compromises on carried interest "makes a mockery of the basic fairness concept in taxation." Beale posits that both chambers of Congress understand that carried interest provides preferential treatment for a very small number of people, and that there is no way to justify such treatment. A failure to pass strong legislation to close the carried interest loophole is further evidence of shady dealings between special interests and our lawmakers.

The carried interest debate is but one of many, many tax debates in the pipe for the year. As with any rule or practice that's been deeply ingrained in our government or society, change becomes a battle of inches. Twenty-five billion dollars over 10 years may not be enough to leap all of our country's many economic hurdles, but it could certainly make life a little less of a struggle for millions of Americans, instead of more lavish for a few.

Financial Reform Conference Committee Excitement

Over at The American Prospect, Tim Fernholz provides a thorough rundown of how the financial reform conference committee will work. The whole piece is worth reading. If you don't have time, here's one key point:

The committee will use the Senate bill, with a few House-bill substitutions, as the default working text, which gives an advantage to reformers, since the Senate bill -- which includes the Volcker rule and tough derivatives-reform provisions -- is stronger than the House bill.

The final bill is likely to be far closer to the Senate version than the House bill, because the unified bill will again need to clear the 60 vote hurdle in the Senate but will only need a simple majority in the House.

Some key points of what is in and what will be debated are below:

Consumer Protection is in and will stay there, but whether it's a standalone Agency (as in the House bill) or a Bureau housed at the Fed (as in the Senate version) is up for debate. The likely outcome is that this hot button issue will hew closely or exactly to the Senate version in order to hold the coalition of Senators necessary to prevent a filibuster. A standalone agency is preferable, but the inclusion of meaningful protection for consumers of financial products looks like it will be one of the major victories of this effort. It's not time to celebrate until the bill is signed into law. Thanks are due to our members who raised their voices in support of it and to all of our coalition partners for getting it this far.

Say on Pay is in as well. There is nothing in either bill that will directly and concretely end the worst excesses of CEO pay and bonuses in the financial industry. Say on Pay is at least a step in the right direction. That's why we started sponsoring a series of Say on Pay shareholder resolutions last year. Our coalition helped to build momentum for the right of shareholder to have a say on the pay of top executives at publicly traded companies. It's good news that Say on Pay is about to become the law of the land for finance.

Derivatives Reform is the hottest topic for the conference committee. The Senate bill includes the Lincoln amendment on derivatives that the banks hate and one of the worlds greatest living economists loves. We know Senator Lincoln (D-AR) best for her disturbing pro-Walton stance against common sense and popular opinion on the estate tax. Her strong amendment on derivatives reform was a pleasant change of pace. Whether it makes it through the conference is one one of the more interesting questions for the bill. Whatever the fate of the Lincoln amendment, it is great news that the requirement that derivates be traded through a clearinghouse will almost certainly make it into the final bill.

More Details: Annie Lowrey has the schedule. And the Washington Post put out a nice summary of some of the differences to be resolved between the House and Senate bills. Mike Konczal has an excellent summary of some keys to what's at stake in the conference committee.

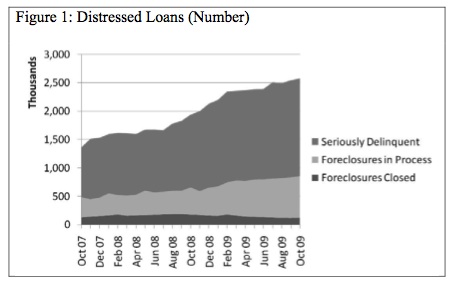

Foreclosures: Case Not Closed

Photo credit: DavidDubov

The US foreclosure crisis was cause for mass hysteria leading up to the 2008 financial meltdown, and the crisis continues to this day. Despite that, the mainstream media has recently largely ignored widespread foreclosures and the deceptive and racially-discriminatory financial practices behind many of them.

Being that the housing bubble was the flimsy core of this Great Recession—and it has resulted in the biggest loss of wealth to communities of color in US history, we’d like to see this issue paid all due attention.

Today, we’ve got the good, the bad and the ugly on the foreclosures situation. We’ll start with the ugly so we can end on a high note.

The ugly: Subprime loans were at the epicenter of the initial stage of the foreclosure crisis, and even now, foreclosure rates are holding steady at high levels that are not expected to drop any time soon. Last month, we learned that one-tenth of all US mortgages are delinquent. Of those who’ve managed to hold onto their homes, one in four is “underwater,” meaning they owe more than their house is actually worth (January 2010 data).

Chart h/t Rortybomb

Communities of color are most impacted by this prolonged crisis, because high-cost home lending was racially targeted. People of color—including many who solidly qualified for prime-rate loans—were over three times more likely to receive a subprime loan than whites. Many banks are engaging in loan modifications, but more than 70% of those modifications are leaving homeowners with more to owe on their principal, which increases their probabilities of re-default.

The bad: Most of the moratoria on foreclosures have expired, without an effective solution to the crisis in place. Last year, a bill was brought to the Senate advocating for judicial modification of loan principles (also known as “cramdown”). But the banking lobbyists flexed their too-powerful political muscles, effectively cramming down cramdown and preventing the bill from passing.

Seems grim, doesn’t it? Don’t throw your hands up quite yet.

The good: Effective solutions are out there.

Passing judicial modification legislation (or something similar)

would go a long way toward helping homeowners rebuild financially. This is something Sen.

Dick Durbin mentioned as a potential financial reform amendment, but was unable to make good on. Not exactly good news, but there is a sign of hope for future legislation in a few of our nation's largest banks having indicated support for it.

Outlawing certain predatory lending practices would also help. The recent success of the Merkley-Klobuchar Amendment, which would prohibit mortgage lenders and loan originators from receiving hidden payments when they lead homeowners into high-cost loans, and create strong underwriting standards to ensure borrowers are actually able to repay the loans they receive, is promising.

These are important first steps, but there’s much more to be done. We’d like to see extended moratoria on foreclosures, particularly those that are unemployment-induced. We’d also welcome federal stimulus funding that is targeted by level of need to reverse the current trend in which more money is flowing to communities that are less severely impacted by the recession than others.

Ending the foreclosure crisis is of critical importance in restoring the financial stability of millions of struggling Americans and preserving the wealth of those most impacted by the Great Recession.

It's safe to say that we've had our fill of the bad and the ugly. Help make good news by rallying our lawmakers around these sensible (and humane) solutions.

(For more on how to promote a fair recovery, check out these policy recommendations from our report, State of the Dream 2010: Drained.)

Making Our Voices Heard: 2010 Estate Tax Lobby Day

Lobby Day is a long-standing tradition at UFE. This two-day training and event gives UFE and RW members a chance to head down to Washington, DC and let Congress know what’s on their minds when it comes to specific policies up for debate.

Lobby Day is a long-standing tradition at UFE. This two-day training and event gives UFE and RW members a chance to head down to Washington, DC and let Congress know what’s on their minds when it comes to specific policies up for debate.

Lobby Day has been a great way for UFE to engage its supporters of the estate tax in direct action around an issue they care deeply about, and this year is no different. The next six weeks are a critical window of opportunity to stop the extension of estate and income tax breaks for the wealthiest Americans at the expense of vital investment in jobs, education and the environment.

Our 2010 Lobby Day is being co-hosted with Opinion Leaders Advocacy Network (OLAN). OLAN is an allied organization made up of progressive political donors, business leaders, philanthropists, and others who do direct advocacy for the public good on a range of issues. With the fate of the estate tax likely being decided this year, we’re giving supporters an exciting opportunity to persuade key Senators to act now to create a strong and sensible estate tax.

Participants in our previous Estate Tax Lobby Days have found speaking to members of Congress exciting and inspiring. And while it’s too late to attend this year’s Lobby Day, we encourage you to sign on to our mailing list if you’re interested in attending events like this in the future.

We're Detroit-Bound: The 2010 US Social Forum

In the last week of June, a crew of UFE staff and interns will travel to Detroit to join as many as 15,000 activists and organizers at the second United States Social Forum (USSF). The Social Forum, in the words of its organizers, "will provide a space to build relationships, learn from each other's experiences, and share analysis of the problems our communities face, [and] will help develop leadership, vision, and strategy needed to realize another world."

In the last week of June, a crew of UFE staff and interns will travel to Detroit to join as many as 15,000 activists and organizers at the second United States Social Forum (USSF). The Social Forum, in the words of its organizers, "will provide a space to build relationships, learn from each other's experiences, and share analysis of the problems our communities face, [and] will help develop leadership, vision, and strategy needed to realize another world."

More than 1,000 workshops, plenaries, cultural events, and street demonstrations have been organized. UFE will present its highly demanded workshop on the financial crisis: "Bankers, Brokers, Bubbles and Bailouts," and two new workshops in Spanish: "Refugiados Economicos Imigracion: la Desigualdad Economica y sus Raices" and "Entendiendo la Crisis Economica en la Comunidad Latina."

Our partners in the US Solidarity Economy Network (USSEN), which was formed at the 2007 Social Forum and is directed by UFE board member, Emily Kawano, will lead one of fourteen program tracks. USSEN's track will focus on addressing poverty and developing an alternative US economy that prioritizes people and planet over profits.

With income and wealth inequality peaking once again, economic recovery for Main Street low on the power brokers' list of priorities, and unending wars and environmental disasters roiling the globe, the stage is set for a powerful people's movement.

For many of those planning to attend the Social Forum, how to build a broad-based, multi-racial, multi-class, multi-generational, and democratic social movement is the central question. The answer starts with an acknowledgement of the truth in the Forum's theme, "Another World is Possible. Another US is Necessary!"

The Southern Border is Not a War Zone

Photo credit: girltwin

Photo credit: girltwin

Increased militarization of the border will inevitably lead to increased violence at the border. It is already happening, and it is not pretty.

Fourteen year-old Sergio Adrian Hernandez Huereca was shot in the head by US border guards this week. On May 31, Anastasio Hernandez, an undocumented Mexican immigrant was beaten, shot with a stun gun and killed after "becoming combative" while in the custody of US border guards. His death has been ruled a homicide. These horrifying incidents are part of a larger trend that, unfortunately, isn’t surprising.

Arthur Brice of CNN wrote:

"According to the [Mexican Foreign Ministry], the number of Mexicans who have been killed or wounded by U.S. border authorities has increased from five in 2008 to 12 in 2009 and 17 so far this year.

Mark Qualia, a spokesman for U.S. Customs and Border Protection, said he could not comment because he does not know where the Mexican government obtained its statistics.

But Qualia noted there were 799 assaults on border agents from October 1, 2009, through May 31. There were 745 assaults for the same time period in 2007-08 and 658 for the same span in 2008-09, he said. [...]"

The escalating violence on our southern border is the unavoidable result of how we currently manage immigration.

Militarizing the border does nothing to address the factors that lead to migration across the border. It only increases the peril of those driven to cross it and the troops and agents tasked with securing it.

Longer and taller fences and walls won’t block the demand for low-wage workers in the US. Meanwhile, trade agreements like NAFTA allow capital to flow freely across the border, contributing to the deterioration of economic conditions in poorer countries like Mexico.

And, sending more boots and guns to the border will only divert money and resources away from our other national priorities, such as high unemployment, which, despite the claims of anti-immigrant groups, is not caused or perpetuated by immigrants, documented or not.

Until we deal with the economic factors driving migrants to leave their homes and families and place their lives at risk to cross the border, the flow of migrants will not slow. But, under our existing immigration policy–sealing borders and increasing enforcement–death and violence will only continue to climb.

Financial Reform Passed the Senate, A Long Way from Done

On May 21, the Senate voted to pass an overhaul financial regulations in response to the financial crisis that brought on the Great Recession. The House of representatives passed their version of financial reform months ago. Progress is being made, but the job is far from done.

As you may recall, merely passing the two houses of Congress is not all it takes for a bill to become law (or if you're not from the School House Rock generation, this chart shows the lawmaking process about as clearly as it can be presented). Conference committee to combine the House and Senate version, a vote in the House and votes in the Senate on the unified bill remain before financial reform makes it to the President's desk.

{kind=link}

The conference committee schedule has been set in the hope of getting President Obama's signature on a financial reform bill before the July 4th Congressional recess. The first meeting will be this Thursday June 10th. And thanks to the pressure from many reform-minded activists and the public, much of the negotiations will be open to the public and televised. You can watch live at SunlightFoudnation.com with context about committee members top donors.

Whatever the result of the conference committee, the law that emerges will not end the need for systemic reform of the financial industry. The House and Senate bills have many good things in them but leave many of the problems with the financial sector entirely unaddressed.

James Kwak explains the need for financial reform beyond the current measures. He cites Paul Krugman and others in explaining that Congress is doing some good to address the short term problems but is leaving most of the long term structural problems in place. Chief among them is the overall size of the financial sector.

Krugman makes the point clearly in a post featuring a chart of the financial industry share of domestic profit. As the Nobel winning economist puts it:

We got into this mess because we had an over-financialized economy, with finance making a share of profits out of all proportion to its actual economic contribution. And now it’s baaaack.

The current financial reform effort has merits (consumer financial protections and Say on Pay rules to name two). Policy makers needs to pass the bill and get right back to work on cutting the financial sector down to size.

Estate Tax Organizer Lee Farris on the Rick Smith Show

To listen to Lee's full interview on the Rick Smith Show, click here (MP3).

Highlights from the interview:

Farris: "[The estate tax could be called] the dynasty tax. It's the tax so that we don't have dynasties. It's the meritocracy tax, it's the tax that enforces having a meritocracy where you get ahead on your own merits rather than on your parents'.

Under [Presidents] Eisenhower and Kennedy, the very wealthy were paying more than half of their income in taxes. That's not true now. We did it before, there's nothing about now that's different than then. It's just the whole political outlook about what taxes should be like. That's the difference."

America Throws the Gauntlet Down on AZ

America's got a bone to pick with Arizona. The state's anti-immigrant

legislation (SB 1070), signed into law by Gov. Jan Brewer in April,

has caused a nationwide uproar of people who view it as a misguided

political ploy. (It's no secret that this is an election year for

Brewer, and it appears she may have some campaign

funding problems, which may or may not have played a role in this

bold move.)

Not only has the Arizona decision elicited the expected cacophony of advocacy groups challenging the law, but cities across the country, stretching from coast to coast with some in between (including our very own, Boston) have made Arizona's immigration policy their business, making moves to boycott the state and municipalities of Arizona until the decision is reversed.

President Obama has publicly denounced the law (watch it below), advocating for comprehensive immigration reform over punitive and divisive patchwork measures (e.g., fences, walls, community raids, round-ups, detentions and mass deportations).

Obama pow-wowed with Gov. Brewer earlier this month to find common ground on this issue. It was pretty much a waste of jet fuel and air time, because not much came of the meeting. Brewer is holding her ground, saying the completion of the Great Wall between the US and Mexico and increased militarization of the border are prerequisites to comprehensive reform.

Meanwhile, the Department of Justice is reviewing Arizona's immigration law in consideration of a potential suit against the state for violations of civil rights. To that end, Brewer had this to say--she won't go down easy, and is willing to go to some extreme legal lengths to prove her point.

Despite Brewer's incorrigibility on reversing SB 1070, and despite the generally favorable results of full-context-lacking polls about the law, we're able to find clarity in paradox. Most of those who support the Arizona law only do so because it was a form of action on a long-standing concern. At the same time, an overwhelming majority of voters, including those who support the Arizona law, would support comprehensive immigration reform by the federal government. That begs this question: What are our elected officials [still] waiting for?

Unemployment Situation: A Longer Wait Time for People of Color?

Photo credit: Pan-African News Wire

The Bureau of Labor Statistics released updated unemployment numbers for May 2010, and the story hasn’t yet changed…sort of. Nearly one in ten US workers continue to go without work, but the reality is still more unsettling for people of color.

Unemployment for white workers has fluctuated a few tenths of a point in recent months, and now sits at 8.8 percent. Workers of color, on the other hand, are still weathering unemployment storms of double-digit magnitudes. Latino unemployment fell 0.1% from the previous month to 12.4 percent. And, Black unemployment, despite a one-point drop, is still highest of all at 15.5 percent.

It's worth noting that last month's unemployment numbers are slightly distorted due to a rise in temporary government employment for Census 2010. That aside, we should continue bracing ourselves for a long and rough ride back to full employment.

Treasury Secretary Tim Geithner and others in the Obama administration have said we shouldn’t expect a return to a more stable employment situation for a few years, at best. According to Mr. Geithner:

“The worst is behind us...However, the country faces significant and ongoing challenges: high unemployment, the need to build a new and stable foundation for prosperity in the years and decades ahead, and a medium- and long-term fiscal situation that could ultimately undermine future job creation and economic growth.”

Challenges to come, absolutely. But the worst being behind us? That has yet to be seen.

Despite the historic legislative strides made or in process as of late, the voices of well-funded special interests continue to overwhelm those of average Americans, let alone people of color. Latino and Black workers are, respectively, 1.40 and 1.76 times more likely to be out of work than their white counterparts, highlighting that not enough is being done to address the roots of racial economic inequality.

So, when they say stability is still a few years away, what does that bode for communities of color? How long will they have to wait?

Until the administration and Congress get serious about enacting economic policies that will truly serve those in need, and not pandering to the desires of moneyed interests, that “foundation for prosperity” won’t be possible – especially for people of color.

We need targeted job creation aimed at employing workers in economic deserts – those communities most devastated by this crisis. We need measures in place that will safeguard consumers from the traps set by financial predators who place families’ economic well being in jeopardy. We need progressive tax policies that will generate revenue for social programs that make recovery and broadly shared prosperity possible. And, we need these types of policies to start now.

How Unfair Tax Breaks Benefit the Richest Americans

Work vs. Wealth

How Unfair Tax Breaks Benefit the Richest Americans

By Brian Miller

Originally published in the Fayetteville Daily News, June 1, 2010

Now that the dust has settled from this year's tax-filing scramble, here are a few facts to keep in mind as Congress moves closer to debating the expiring Bush tax cuts. By the end of 2010, those cuts, which began to take effect in 2001, will have cost our nation $2.5 trillion dollars.

To put that enormous loss of revenue into perspective, consider this: It's twice as much as the combined cost of the wars in Iraq and Afghanistan. And it's two-and-a-half times the cost of the recently passed health-care plan.

Nearly half of those costly Bush tax cuts went to the top 5 percent of households. But instead of the promised trickle-down growth, we got stagnant wages for middle-class Americans while many wealthy households grew even wealthier. Over the last decade, a record federal budget surplus--before the Bush tax cuts--has turned into a massive federal deficit.

I recently spoke on a radio show about the work of Responsible Wealth, a network of American millionaires speaking out in favor of higher taxes on the wealthy. These millionaires want to dial back the portion of Bush tax cuts that benefited the top 5 percent, which includes people like themselves, while preserving the tax cuts for low and middle-income families. What's more ironic is that they're pledging to give away their savings under the Bush tax cuts to groups that are working to end those and other tax breaks for the wealthy.

I shared a story about one of those millionaires--he has an income of over half a million dollars per year, but pays less than 15 percent of those earnings to the IRS. The host and callers were all outraged, and rightfully so. But, their initial instinct--to direct their outrage at this millionaire for "gaming the system"--was misguided. He's not the one gaming the system. The Bush administration did it for him.

A lot of Americans look at the federal income tax, of which the top rate is 35 percent, and think that if someone like this millionaire is taxed at such a low rate, he must be cheating. Here's how it's possible: that 35 percent top rate only applies to earned income. While he's well paid as a professor, three-fourths of his total income is in the form of capital gains and dividends from a sizeable investment portfolio. (Some was inherited and some was built up during his days as an investment banker.) And the top rate for capital gains and dividends is only 15 percent.

In short, money earned through work is taxed at a higher rate than money made from, well, money.

The intense focus by the media and anti-tax groups on the federal income tax is preventing too many people from seeing the true size of the tax giveaways bestowed upon our nation's wealthiest households. It's like the ship's crew pointing at the tip of the iceberg, but ignoring the hulking mass beneath.

For most Americans, wages and salaries account for roughly 80 percent of their total income, but that ratio starts dropping sharply for those earning over $200,000 per year. For many with incomes of $1 million or more per year, about 25 percent is from wages and salaries; the rest is primarily passive income, like capital gains and dividends. By taxing investment income at a lower rate than earned income, we've tilted the system heavily in favor of the rich.

For a country that prides itself on the hard work of its citizenry, we seem to have lost our way. It's unacceptable that those who have gained the most from our society, and who have the most to give back, are actually paying taxes at a lower overall rate than most others. We need to start taxing money-from-money income at the same level as the earned income that most Americans depend on. Ending the Bush tax cuts for the wealthiest households, which includes restoring the top capital gains and dividends rates to their pre-Bush levels, is an essential first step.

Quick Reactions: Senate Passes Financial Reform

- Paul Krugman likes what the Senate did. He links to and agrees with Edmund Andrews.

- David Leonhardt sees areas for improvement.

- Simon Johnson is less than thrilled.

- Next step: conference committee to combine the Senate bill with the House version.

Raise My Taxes, Please!

![]()

"I am a wealthy American who supports higher taxes on wealthy people. I realize that agitating to pay more taxes is unusual. When I appeared on Fox News recently, the host, Neil Cavuto, opposed my position but also called me an altruist with a good heart, because I favored a policy against my own self-interest. I thank Neil for his kind words, but I disagree with him. I believe higher taxes on myself are in my own self-interest.

"I am a wealthy American who supports higher taxes on wealthy people. I realize that agitating to pay more taxes is unusual. When I appeared on Fox News recently, the host, Neil Cavuto, opposed my position but also called me an altruist with a good heart, because I favored a policy against my own self-interest. I thank Neil for his kind words, but I disagree with him. I believe higher taxes on myself are in my own self-interest.

Although repealing the Bush tax cuts for the wealthy will cost me a lot, I think doing so is necessary to address a looming national debt crisis that could severely harm me and my family. In the face of this threat, I consider it perfectly self-interested to worry more about the state of the overall national economic pie than about my own particular slice. [...]"

Read the full op-ed by Responsible Wealth member Eric Schoenberg

WA State: Can We Get an "Amen!" for Fair Taxes?

This summer, a Washington state coalition of businesses,

labor and social justice organizations, and a few prominent civic leaders,

including our friend, Bill

Gates, Sr., is trying to make history. They’re putting boots on the streets

to advance to the November ballot Washington’s

first tax reform initiative in 40 years. The message of the initiative, I-1098, is simple: Washingtonians are

suffering from the state’s budget crisis, and they are in desperate need of a

fair tax code to fund core public services like education and healthcare.

This summer, a Washington state coalition of businesses,

labor and social justice organizations, and a few prominent civic leaders,

including our friend, Bill

Gates, Sr., is trying to make history. They’re putting boots on the streets

to advance to the November ballot Washington’s

first tax reform initiative in 40 years. The message of the initiative, I-1098, is simple: Washingtonians are

suffering from the state’s budget crisis, and they are in desperate need of a

fair tax code to fund core public services like education and healthcare.

One coalition member, Washington Community Action Network (also a member of UFE’s Tax Fairness Organizing Collaborative), will host a launching event for volunteers this Memorial Day weekend on Saturday, May 29th to start getting the word out and gathering signatures of Washington voters.

Forty thousand residents have lost basic health coverage as a result of the state’s fiscal woes. That includes thousands of seniors and disabled residents who have lost daily care, and children who may be susceptible to illness due to elimination of state-funded vaccinations. On education, a seventy percent reduction in funds to reduce class sizes is causing classrooms to bulge with more, and presumably less engaged, students.

The passage of I-1098 would restore funding to those services while, at the same time, lowering taxes for the majority of Washington households. Sounds oxymoronic, right? That’s the beauty of a progressive tax structure – a fair share of the costs of public services are paid for by those who’ve benefitted the most from them, and who, in turn, have the most to give back to the common good. Here’s an overview of I-1098:

- It reduces the state property tax by 20%.

- It increases the small business tax credit from $420 to $4,800 annually, eliminating the state business and occupation tax for more than 80% of businesses, and reducing taxes for another 10%.

- And, here’s where the added revenue comes from: The top 3% wealthiest households in Washington will pay a new income tax. Married couples will pay just 5% on incomes over $400,000 ($200,000 for singles), and 9% on incomes over $1 million ($500,000 for singles). The new tax would raise about $1 billion – with a “b” – annually, even with the small business and middle-class tax cuts.

For those who are still on the fence about whether this sounds fair, consider this: The wealthiest Washingtonians currently pay less in state and local taxes than their counterparts in 43 other states. Washington has the most regressive tax system in the country, with households in the top 1% paying a mere 3% of their income toward state and local taxes, while those in the bottom 20% pay 17 percent.

Asking for a little more from the top 3% (about 83,700 out of 2.27 million households) isn’t too much when we’re talking about the well being of over 6.6 million people.